MRED Blog

REinventing MLS

Category Archives: Mortgage

Rent vs. Buy: Either Way You’re Paying A Mortgage

There are some people that have not purchased a home because they are uncomfortable taking on the obligation of a mortgage. Everyone should realize that, unless you are living with your parents rent free, you are paying a mortgage – either your mortgage or your landlord’s.

As The Joint Center for Housing Studies at Harvard University explains:

“Households must consume housing whether they own or rent. Not even accounting for more favorable tax treatment of owning, homeowners pay debt service to pay down their own principal while households that rent pay down the principal of a landlord plus a rate of return.

That’s yet another reason owning often does—as Americans intuit—end up making more financial sense than renting.”

Christina Boyle, a Senior Vice President, Head of Single-Family Sales & Relationship Management at Freddie Mac, explains another benefit of securing a mortgage vs. paying rent:

“With a 30-year fixed rate mortgage, you’ll have the certainty & stability of knowing what your mortgage payment will be for the next 30 years – unlike rents which will continue to rise over the next three decades.”

As an owner, your mortgage payment is a form of ‘forced savings’ that allows you to have equity in your home that you can tap into later in life. As a renter, you guarantee your landlord is the person with that equity.

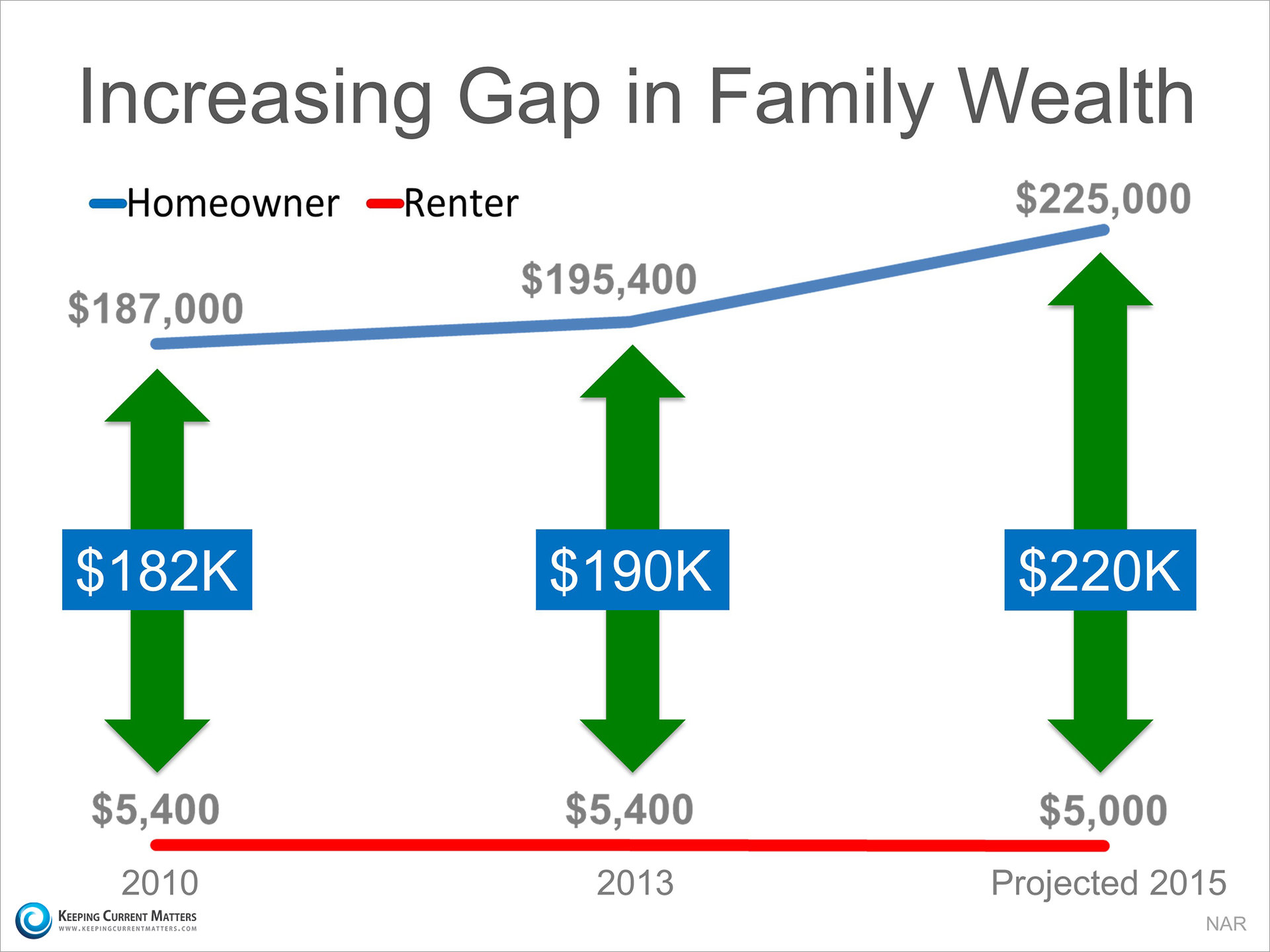

The graph below shows the widening gap in net worth between a homeowner and a renter:

Bottom Line

Whether you are looking for a primary residence for the first time or are considering a vacation home on the shore, owning might make more sense than renting with home values and interest rates projected to climb.

Blog post via KCM Blog

3 Promising Graphs on the Nation’s Mortgage Market

It’s been roller coaster ride following the nation’s mortgage markets, so Chicago Agent Magazine decided to take a more long-term view at some of the key stats at play – and how, with only one exception, things have improved quite a bit.

It’s been roller coaster ride following the nation’s mortgage markets, so Chicago Agent Magazine decided to take a more long-term view at some of the key stats at play – and how, with only one exception, things have improved quite a bit.Why Have Interest Rates Dropped?

The headlines agree mortgage interest rates have dropped substantially below initial projections. Many who are considering purchasing a home, or moving up to their dream home, might think that they should wait to buy, because rates may continue to fall.

A recent article on the Economists’ Outlook blog by the National Association of REALTORS® (NAR) provides insight into one major factor in the decline in interest rates, the crude oil price.

“As of January 5, 2015, the U.S. Energy Information Administration (EIA) reported that the price of regular gasoline was $2.20/gallon, the lowest since gas prices peaked to about $ 4/gallon in May 2011.”

You may have noticed that filling your gas tank has become substantially less expensive in recent months. A welcome change from the close to $5 a gallon that many Americans were paying this time last year. The average US household is projected to save around $550 in 2015.

So what does that have to do with Interest Rates?

NAR explains the correlation like this:

“Lower oil prices mean lower inflation rate, which pushes down mortgage rates.”

Based on Freddie Mac’s weekly mortgage survey as of January 22, 2015, the 30-year fixed rate averaged 3.63% and the 15-year fixed rate averaged 2.93%.

“The decline in oil prices is generally positive to households by way of the gas savings and lower mortgage payments. That savings will boost consumer spending in other areas. But there may be some layoffs in oil-producing states.”

How long will rates stay low?

No one really knows how long oil prices will continue to support low mortgage rates. In a New York Times article, the author points to the fact that “adding hundreds of billions of dollars to consumer spending” could start to have a “counter effect” on rates as the economy continues to strengthen.

“If firms start hiring again, and wages increase — that’s when the level of all interest rates in the U.S. would increase.”

Don’t wait too long

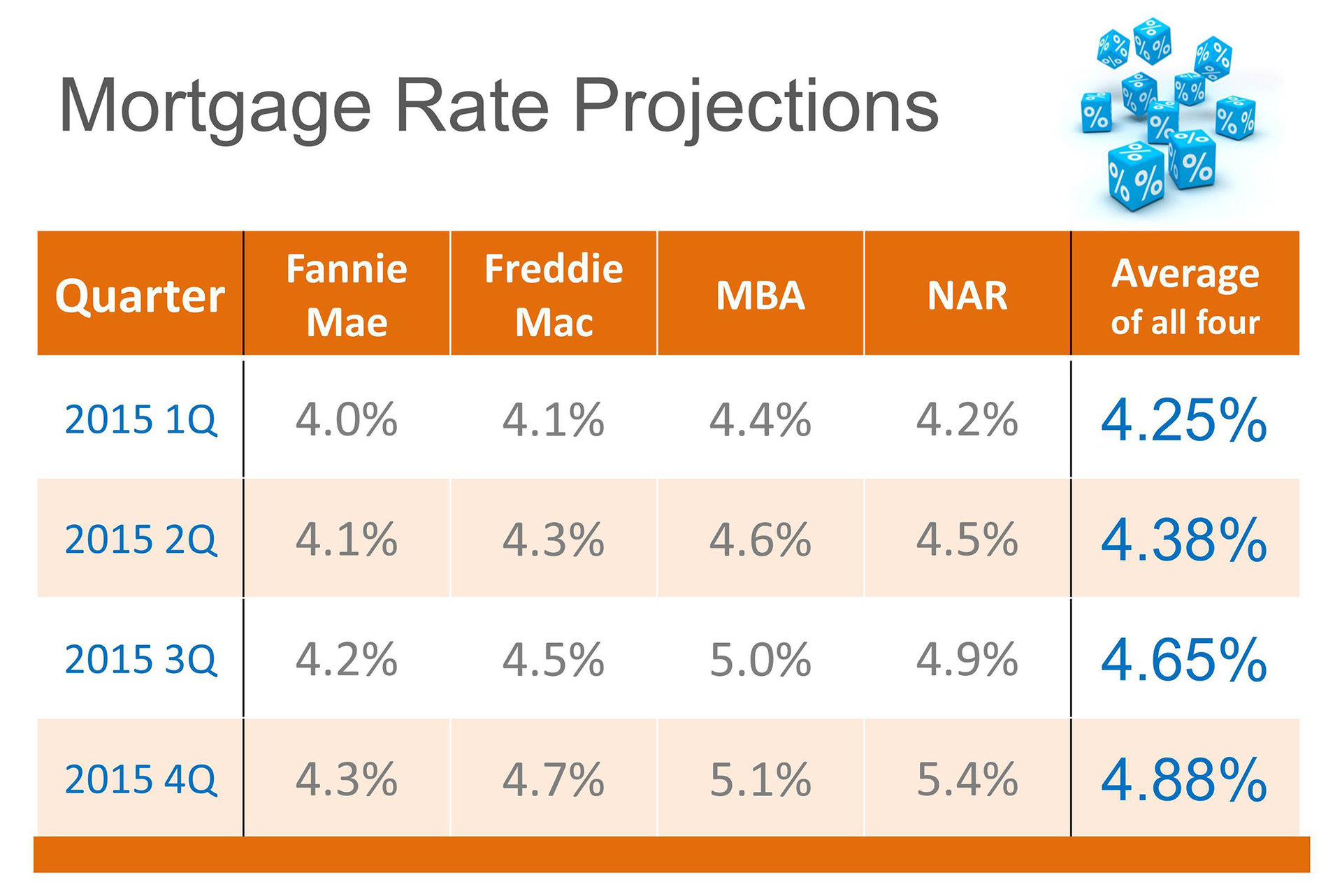

The low interest rates we are currently experiencing are not going to stay around forever. The current projections from Freddie Mac, Fannie Mae, NAR and the Mortgage Bankers Association all agree that interest rates will increase to between 4.3-5.4% by the end of 2015.

Bottom Line

NAR reports: “At the median home price of $205,300, a 0.75 percentage point drop in mortgage rates will yield savings of about $1,000 annually.”

If you are in a position to buy a home make sure that you meet with a local real estate professional with their finger on the pulse of what’s going on in the market. Don’t let a delay in purchasing impact your family’s financial future.

Blog Post via KCM Blog

Where will Mortgage Rates be Headed in 2015?

We finished 2014 with the 30 year fixed mortgage rate at 3.87% as per Freddie Mac. This is very close to the historic lows in the spring of 2013.

However, the Mortgage Bankers Association projects mortgage rates to be about 5% by the end of 2015. The website Investopedia agrees and gives some perspective on the 5% rate:

“Barring another financial and housing market implosion, and if the economy continues to improve, expect interest rates to rise in the latter half of 2015. If they do jump to the 5% range it will be a modest hike when compared to historical averages. Rates will still be far below the approximately 8.5% 30-year fixed-rates mortgages have averaged since 1971 when Freddie Mac started tracking them. Rates averaged 6% in the years leading up to the recession.”

Here are the latest 2015 mortgage rate projections from Fannie Mae, Freddie Mac, the Mortgage Bankers’ Association and the National Association of Realtors:

Blog post via KCM Blog