MRED Blog

REinventing MLS

Category Archives: Agent “Doing Business” Discussions

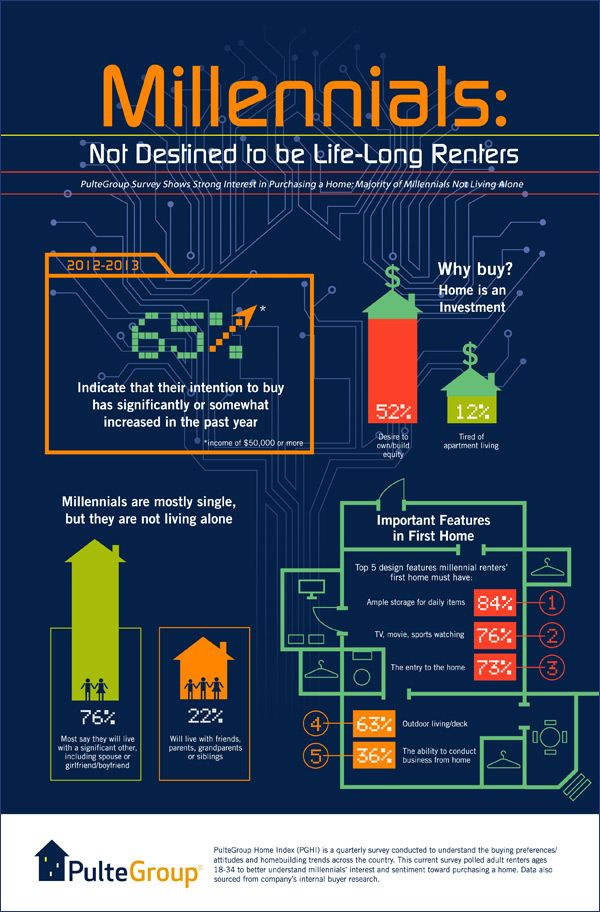

Millennials: Not Destined to be Life-Long Renters [Infographic]

This infographic shows how Millennials show a strong interest in purchasing a home via the KCM Blog

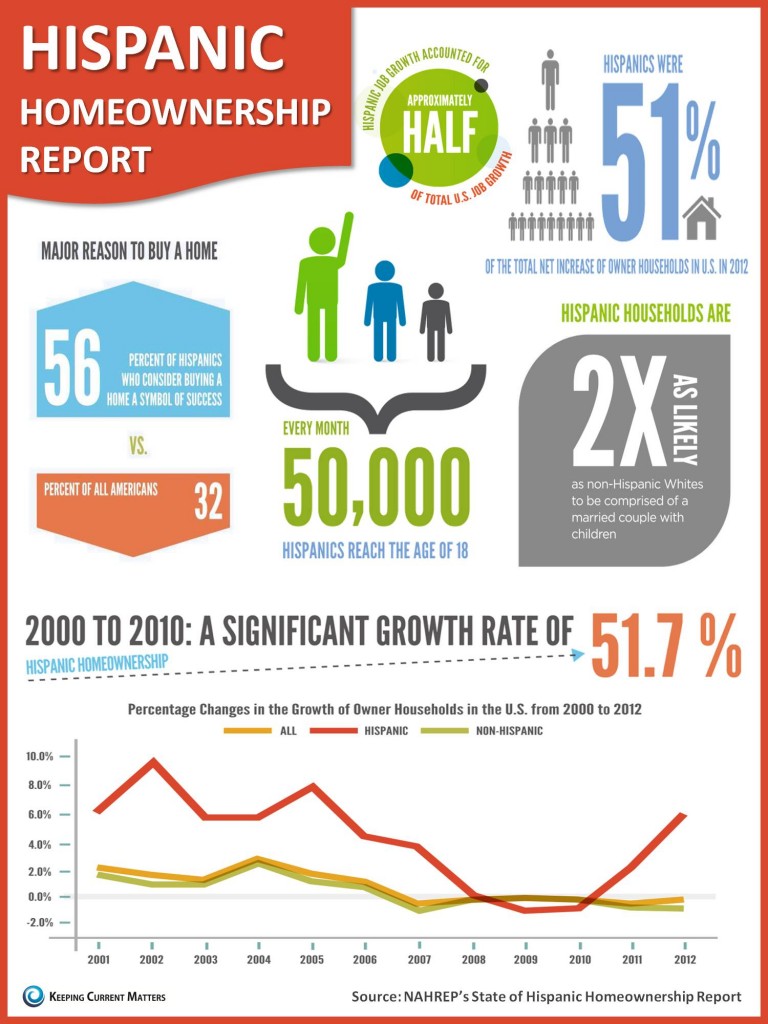

The State of Hispanic Homeownership [Infographic]

Infographic from the KCM Blog

NAHREP: State of Hispanic Homeownership Report

The National Association of Hispanic Real Estate Professionals’ recently released their The State of Hispanic Homeownership Report. The 24-page document offers an update on the Hispanic homebuyer market and traces Hispanics’s rise in household formations and reveals the variables that make them homeownership-ready and able to drive demand in the current homebuyer market.

According to the report, Hispanics continue to lead the surge in U.S. homeownership and accounted 51% of the total net increase of owner households. The number of Hispanic homeowners grew from 4.24 million in 2000 to 6.69 million in 2012, a remarkable increase of 58 percent at a time when the rest of the U.S. population saw a net increase of only 5 percent.

Read some of the key statistics highlighted in the report via the KCM Blog

4 Common Down Payment Assistance Program Myths Debunked

Today’s homebuyers are doing significant online research before beginning their home buying search, yet there are still many misconceptions about home financing and down payment assistance programs. Home prices, along with down payments, are increasing, and assistance programs can help make buying a home as affordable as possible.

Are these common myths keeping you from investigating homebuyer assistance options?

Myth #1: Down payment assistance programs are only for first-time homebuyers.

First-time homebuyers are defined as someone who has not owned a home in three years. And, not all programs specify that you must be a first-time homebuyer. It’s important to know that assistance programs are for homebuyers, not investors. Most housing agencies will require that the home is occupied as a primary residence in order to qualify.

In addition, homebuyers purchasing a home in a designated target area (typically for revitalization efforts) may receive special benefits such as higher assistance amounts, more lenient income requirements and the first-time homebuyer requirement may be waived. Veterans are often eligible for a first-time homebuyer waiver, too!

Myth #2: Assistance programs are no longer funded.

There are many public and private-funded programs available. In fact, there are hundreds of millions of dollars in down payment assistance, tax credits, affordable fixed-rate mortgages and rehab loans available throughout the country.

Each program has a different funding schedule. Some programs are government-funded and are provided through municipal or quasi-government agencies or non-profits. Others are privately funded, and some are even sponsored by employers. Every state has a collection of programs at the state-level, and hundreds of markets around the country offer local assistance as well.

Watch this four-minute video to learn about the three most common types of homebuyer programs.

Myth #3: It’s difficult to qualify for homebuyer programs.

There are many options and opportunities. The key is doing research early in the home buying process as well as reviewing the application criteria.

To qualify for an assistance program, the homebuyer and the property will have to meet certain criteria, which vary by program. Standard criteria include property location, type of home, sales price limits, household income thresholds, and homebuyer education certifications. There are often additional benefits, or even entirely separate programs, for educators, protectors, health care workers, veterans of the armed forces, and households with disabled members.

Down Payment Resource gives homebuyers the opportunity to answer a few simple questions to determine if they may meet the basic qualifications for a program.

Homebuyers must also demonstrate that they are financially responsible. Assistance programs have credit score thresholds and cash reserve requirements. Most programs will require a little money down from the homebuyer, as well as homebuyer education, especially for first-time homebuyers, to ensure the long-term homeownership success of each new buyer.

Myth #4: Using a down payment assistance program makes home financing more difficult.

Homebuyer program administrators often train “participating lenders.” These are lenders who are qualified to write the loans associated with the programs and understand how to incorporate this special financing into the home loan without complicating or prolonging the real estate transaction. This is why it’s important for homebuyers to seek information about available programs prior to touring homes or even getting prequalified. A little homework upfront ensures a smooth, successful transaction down the road.

You can begin by visiting your state’s Housing Finance Agency website to discover available programs. You can also use Down Payment Resource to access the participating lenders for specific programs.

Down payment assistance can help boost homebuyers’ purchasing power, help buyers retain a solid cash reserve for home improvements and other moving costs, and revitalize our communities with more homeowners.

Article via Down Payment Resource

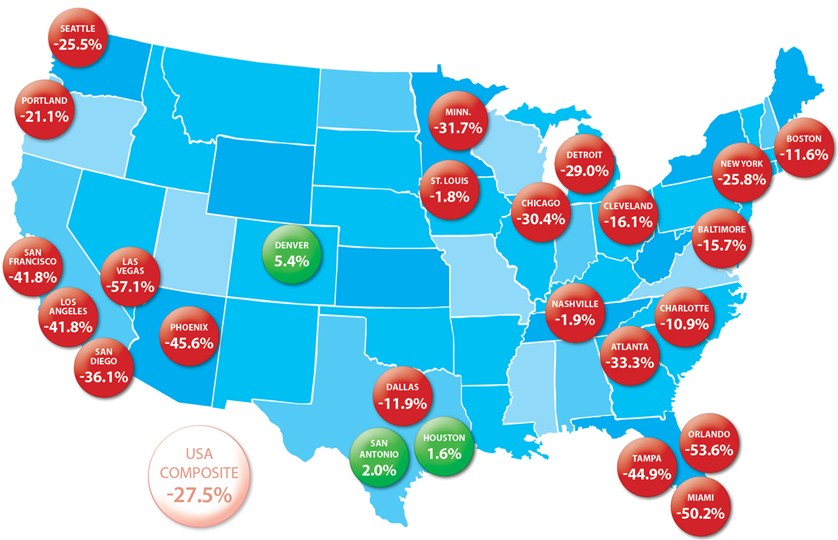

Homes ‘On Sale’ Across the Country [Infographic]

Prices are increasing but are still ‘on sale’ throughout most of the country when compared to 2007 prices. Infographic via KCM Blog

Prices are increasing but are still ‘on sale’ throughout most of the country when compared to 2007 prices. Infographic via KCM Blog

RealtyTrac: Foreclosure activity rising in 2013

In its first-ever U.S. Foreclosure Inventory Analysis, RealtyTrac revealed that 1.5 million U.S. properties were actively in the foreclosure process or bank-owned in the first quarter of 2013.

This number was up 9% from the first quarter of 2012, but still down 32% from 2.2 million in December 2010, which represents the peak.

“Delinquent loans that fell into a deep sleep after the robo-signing controversy in late 2010 are gradually coming out of hibernation following the finalization of the national mortgage settlement in April 2012,” said Daren Blomquist, vice president at RealtyTrac.

Blomquist notes that the settlement provided some closure regarding accepted foreclosure processing practices, and as a result lenders have been reviving more of these delinquent loans and pushing them into foreclosure over the past 12 months, particularly in states where a lengthy court process has resulted in a bigger backlog of non-performing loans still in snooze mode.

According to data from RealtyTrac, the yearly increase in foreclosure activity nationwide was due to a 59% spike in pre-foreclosure inventory. However, the pool of homes scheduled for foreclosure action dropped 25% and inventory of bank-owned homes fell 3%.

Inventory behavior fell nearly even, with 26 states reporting annual increases in foreclosures, while 24 states (along with the District of Columbia) posting annual decreases, the data shows.

Excluding bank-owned properties, 35% of properties actively in the foreclosure process sat vacant.

Listed foreclosure inventory plummeted 43% nationwide from year-ago numbers, while unlisted inventory rose 12%.

Article via Housingwire